The Department of Legislative Services (DLS) today presented its annual fiscal briefing to the General Assembly budget committees. This briefing provides a comprehensive overview of the Governor’s proposed FY 2021 operating and capital budgets, aid to local governments, and the State’s economic and revenue outlook.

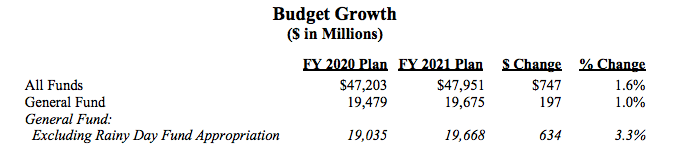

The Quick Look at Fiscal 2021 Budget shows that the Governor’s proposed budget leaves a general fund balance of $414.4 million at the end of FY 2020 and $108.5 million at the end of FY 2021. The Rainy Day Fund ends FY 2021 with a balance of $1.2 billion (6.28% of general fund revenues). Combined cash balances at the close of FY 2021 of $1.3 billion equal 6.8% of general fund revenues.

The Spending Affordability Committee (SAC) set a goal of eliminating the structural deficit forecast for FY 2021. The Administration’s budget reduces but fails to eliminate the structural gap for FY 2021, leaving a structural deficit of about $37 million.

DLS forecasts a structural deficit of $701 million in FY 2022 and $1.1 billion (5% of general fund revenues) by FY 2025. The shortfalls are exacerbated by the Governor’s plan to allocate $1 billion of general funds to transportation needs and targeted tax relief from FY 2021 through FY 2025.

The enhancements to school construction and K-12 education that the General Assembly will consider during the session represent significant state investments which, if not supported by an ongoing funding plan, will exacerbate the structural deficit.

Budget Reconciliation and Financing Act

The Administration’s balancing plan rests on a Budget Reconciliation and Financing Act (BRFA) (HB 152/SB192) that reduces general fund spending by $530.6 million and generates $157 million of revenue.

SDAT Cost Shift

The BRFA revives an attempt (unsuccessful in previous years) to shift costs of the State Department of Assessments and Taxation (SDAT) onto county governments.

The BRFA proposes increasing counties’ reimbursement of SDAT functions, including costs of real property valuation, business personal property valuation, and information technology. Since 2013, counties have reimbursed the state for 50 percent of the costs for these functions, but the BRFA proposes increasing this share to 60 percent, permanently.

This proposed permanent cost shift not only imposes a high fiscal burden on counties, but threatens the objective nature of having assessment functions managed and funded by an entity that does not meaningfully, directly benefit from the results of those assessments. Having assessments conducted by the State, rather than the counties, helps assure taxpayers that the assessing body provides objective, unbiased analysis.

Previous Conduit Street Coverage: It’s Back! Governor Revives SDAT Cost Shift To Counties

Community Colleges

In Governor’s FY 2021 proposed budget, community colleges are funded through the John A. Cade formula at $268 million. While this is a 7.3% increase compared to FY 2020 funding, it is actually less than would have been dictated by the Cade funding formula (by $18.2 million).

The BRFA proposes to amend the standard formula to limit the growth of community college funding. Beginning in FY 2022, funding for community colleges is limited to the FY 2021 appropriation plus the annual percentage increase in General Fund revenues above the estimated annual increase in General Fund revenues, which is calculated by the Board of Revenue Estimates.

DLS estimates that this proposal would cut overall funding for community colleges by approximately $100 million by FY 2025.

Baltimore City Share of Highway User Revenues

The BRFA proposes to divert $5 million for FY 2021 through FY 2024 from the Baltimore City share of Highway User Revenues (HUR) to the Maryland Department of Transportation (MDOT) to support capital improvements for the Howard Street Tunnel.

Revenue Volatility

State law requires that the Revenue Stabilization Account or the Fiscal Responsibility Fund receive a share of nonwithholding general funds above a cap that is based on the 10-year average nonwithholding revenues’ share of total general funds. Revenues from the Fiscal Responsibility Fund may only be appropriated in the second following fiscal year to PAYGO capital projects for public school construction, public school capital improvement projects, capital projects at public community colleges, and capital projects at four-year public institutions of higher education.

The BRFA proposes to changes the cap on the adjustment to general fund revenues related to the nonwithholding income tax revenue to dollar amounts rather than a percent of general fund revenue, beginning with $60 million in FY 2021, and slows the full phase in to a 2% cap until FY 2026 rather than FY 2022.

State Aid to Local Governments

State aid to local governments increases by $291.8 million over FY 2020, most of which is in the form of education, aid, which increases by $212.9 million, or 3.0 percent. Community college aid increases by 18.4 million, or 5.5 percent ($18.2 million less than what is dictated by the Cade funding formula); transportation aid increases by $8.3 million, or 3.2 percent; aid for libraries increases by $0.7 million, or 0.8 percent; public safety aid increases by $35 million, or 23.6 percent (this is primarily due to an increase in the state 9-1-1 fee for the purpose of accelerating the transition to Next Generation 9-1-1); disparity grant aid increases by $12.1 million, or 8.3 percent; and local health grants increases by $0.9 million, or 1.6 percent.

Previous Conduit Street Coverage: Governor’s 2021 Budget Proposal – What It Means for Counties

Fiscal 2021 Capital Budget

The capital budget provides $1.095 billion of new general obligation (GO) bonds which is consistent with the level programmed in the 2019 Capital Improvement Program (CIP) for FY 2021 and the level recommended by the Capital Debt Affordability Committee (CDAC) and the SAC.

The level of GO bond funds programmed in the 2020 CIP exceeds the limits established by both CDAC and SAC by $50 million in each of FY 2022 through FY 2025 for a total of $200 million through the planning period.

Economic and Revenue Outlook

Stay tuned to Conduit Street for more information.